Today the threshold for HECS-HELP repayment was lowered from $55,874 to $51,957, as a result of a bill passed in 2016.

While many were expecting the threshold to be lowered to $45,000 (insert media frenzy), parliament failed to get the bill passed before finishing for the year—if it passes when they return in August, it is unlikely to come into effect until July 1, 2019.

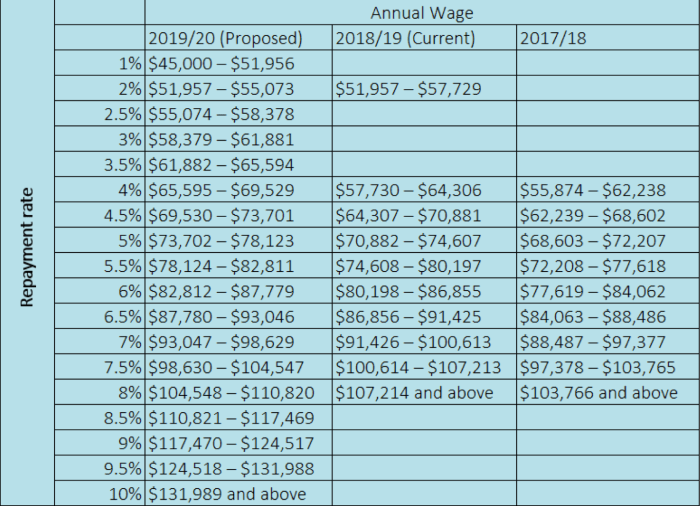

Depending on how much you’re earning, the changes effective as of today will affect you in different ways.

Previously, you would start paying your HECS debt back once you reached an annual income of $55,874; with a repayment rate of four per cent you would be repaying $2234 a year (outrage).

As of today, the threshold has been lowered to $51,957—but, the rate at which you have to pay it back has also been lowered (please explain).

Instead of having to cough up four per cent of your income in the lowest wage bracket, the rate has been halved to two per cent. So, those earning in between $51,957 to $57,729 a year will pay from $1,039 to $1,154.

Those people earning $55,874 (the previous threshold) will now have to pay back less—instead paying back $1,117 (half as much as the previous year).

But let’s talk about those effected by the new threshold.

Those of you on an annual wage of $51,957 will have to pay $1,039 a year towards your HECS debt.

But don’t worry, you won’t be getting hit with the full amount at the end of the year—your employer should be taking it out of your wage (if you’ve told them), which would be about $20 a week.

That’s equivalent to four or five coffees, three or four pints, or one packet of cigarettes.

And yes, you would definitely rather be spending that money on goods and services, but let’s try to put it into perspective.

There are countries where people actually try to fake their deaths to get away from their crippling student loan debt (I’m looking at you America).

Let’s not forget that the HECS-HELP program provides students with an interest free loan (unlike the commercial loans offered to students in the United States), and while we’d all love free education, the Australian government is already at a loss because of outstanding HELP debt.

In the 2016–17 financial year, 2.7 million people had outstanding HELP debts. That year the amount of debt outstanding was estimated to be $54 billion.

It is now estimated to be nearly $52 billion and is forecast to reach $75 billion by 2020–21.

Part of the problem is that some people will never reach the threshold—making it unlikely that they will ever repay their HELP debt.

So, it’s no surprise that the Australian Government was trying to lower the threshold again.

Although their plans to bring in the $45,000 threshold for the 2018/19 year were foiled by the bells of parliament, the new bill is likely to pass when school returns in August.

These proposed changes would likely come into effect on July 1, 2019.

Those in the new lowest annual wage bracket—$45,000 to $51,956—will pay back their HELP loan at one per cent.

This ends up being $450 to $519 a year, or $8.65 to $10 a week.

The proposed changes take a more gradual approach to paying back your HELP debt.

In previous years, you would be paying it back at four per cent, with repayment percentages climbing steeply thereafter.

With these changes, repayment would start at a lower annual wage, but the repayment rate would again be lowered—leaving many full time workers better off.

Instead of focusing our efforts on protesting threshold reductions, it might be wiser to encourage the government to bring back discounts and encourage debtors to pay back in lump sums.

So, let’s put down the pitchforks (for now), because in looking at the bigger picture, these changes could be better for everybody.